High level, here's what you need to know:

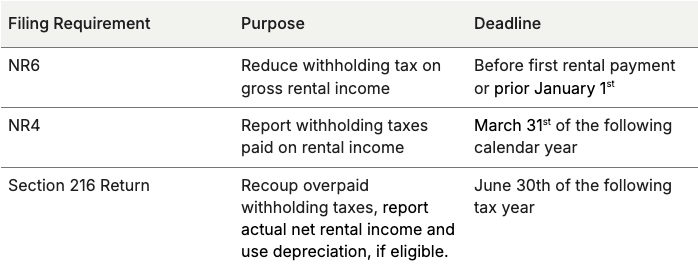

Before collecting rental income, non-resident owners can file a NR6 form with the Canada Revenue Agency (CRA). This form allows you to request reduced withholding tax by your agent based on estimated net rental income rather than gross rental income.

Deadline:

File before the first rental payment of the year or before receiving any rental income. If approved, your agent (often your property manager) withholds 25% of your net forecasted rental income, instead of 25% of the gross.

For all subsequent taxation years, the NR6 form will have to be resubmitted to CRA prior January 1 for approval.

An NR6 is not required to start renting your unit, but without an approved NR6, your agent will be required to withhold 25% of your gross rental income.

If your NR6 is approved, your agent must remit 25% of your net rental income to the CRA monthly. If you do not file an NR6, they must withhold and remit 25% of gross rental income each month.

If you fail filing by June 30th, you will be liable for a penalty corresponding to 25% of the gross rental income, plus 10% penalty, plus interest.

Compliance: The Cornerstone of STR Profitability

For non-resident owners, tax compliance isn't just about avoiding penalties; it's about maximizing your return on investment. With the help of your agent and a knowledgeable Canadian accounting professional, you can effectively minimize your tax burden and as much rental income as possible.